Fit for 55? The impact of the EU’s climate package on the aviation industry

What will be the impact of the EU’s Fit for 55 package on European aviation? The policies are likely to affect passenger demand, fares and emissions, but a number of questions remain over potential distortions and how the policies can help to achieve ambitious net zero targets. Oxera was asked to assess this topic for ACI EUROPE, the trade association representing airports across the Europe region.

This article is based on a report commissioned by ACI EUROPE. For more information, see ACI EUROPE (2022), ‘“Fit for 55” package risks European socio-economic cohesion without supporting measures, independent study shows’, 8 June (last accessed 24 August 2022). See also Oxera’s report: Oxera (2022), ‘Assessment of the impact of the Fit for 55 policies on airports’, prepared for ACI EUROPE, 30 May (last accessed 26 August 2022).

The EU announced its Fit for 55 policy package on 14 July 2021, with the aim of reducing net carbon emissions to 55% of 1990 levels by 2030, and to 100% by 2050.1 The package covers many sectors, including energy production, manufacturing and transport.

As aviation accounted for 3.7% of total EU emissions and 15.7% of total transport emissions in 2018,2 a number of policies are specifically targeted at this sector, and we summarise these below.3 We note that, while the policies apply only to flights originating or terminating in the EU, the knock-on effects on aviation in the wider European area are likely to be significant.

- Reforms to the Emissions Trading System (ETS). The ETS is the EU’s emission allowances trading scheme. A certain number of emission allowances are allocated and/or auctioned to firms in different sectors, and there is the potential to trade allowances between firms. Fit for 55 proposes a faster reduction in the total number of allowances, as well as a reduction in the number of free allowances granted to the aviation industry, with free allowances to be fully phased out by 2030.4

- A revision of the Energy Taxation Directive (ETD). The ETD sets a minimum level of taxation on fuels. This revision significantly raises the level of taxation, with the changes being brought in over a number of years. Kerosene, which was previously exempt from EU-wide fuel taxes, will be taxed at a rate of €10.75 per gigajoule when the minimum taxation rates reach their full level in 2033.5

- The ReFuelEU Aviation Initiative (‘ReFuelEU’). ReFuelEU mandates minimum proportions of Sustainable Aviation Fuel (SAF) when departing from an EEA airport, with the proportions set at 5% in 2030 and gradually increasing to 63% in 2050.6

- The Alternative Fuels Infrastructure Regulation (AFIR). AFIR mandates that all airport gates must have electricity supplied to stationary aircraft by 2025, and all outfield posts by 2030.7

The Commission’s policies are designed to be consistent with the roll-out of the UN’s CORSIA initiative,8 which aims to offset all growth in emissions from the aviation sector against a baseline of average emissions in 2019 and 2020. The Commission has noted that it will revisit the scope and strength of some of the Fit for 55 policies in light of the future roll-out and stringency of CORSIA. For example, it will assess whether the ETS should cover all flights departing or arriving in the EEA (as it currently applies only to departing flights).9

While the Commission has looked at the impact of some of these policies, it has not undertaken a holistic assessment of their combined impact on the aviation sector. Our analysis looks at the impact of Fit for 55 on airfares, passenger demand and emissions in the European aviation sector, as well as the implications for reaching net zero targets.

What is the impact on fares and passengers?

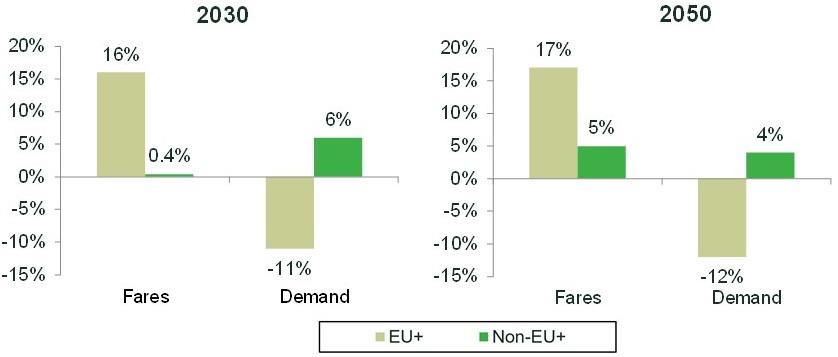

As the policies will be gradually strengthened over the next few decades, we consider their impact at two points in time: 2030 and 2050. We estimate that fares will increase by 11% by 2030 and 13% by 2050, with demand falling by 5% and 6% respectively. These fare increases and declines in demand are estimated relative to a scenario where the policies are not in place in 2030 or 2050, rather than relative to current levels of fares and demand.

The rise in airfares is a result of the effect of the policies on fuel prices. Airlines must pay to emit kerosene by buying credits under the ETS and paying taxes under the ETD. Alternatively, airlines may use SAF as required by ReFuelEU and save on these costs, but pay a higher price for SAF than for kerosene. These increases in costs are then likely to be partially passed through to passengers in higher fares. As these policies fall more heavily on flights between two EU airports than flights between an EU and a non-EU airport, the fare increases are much greater for intra-EU+ flights than for extra-EU flights, as shown in Figure 1 below.10

Figure 1 Impact of the Fit for 55 policies on fares and demand

If fares for intra-EU flights increase, consumers can choose to pay the higher price, not travel at all, travel by another mode of transport (e.g. train), or fly on a similar extra-EU route where the price has not increased to the same extent. This diversion of passengers from intra-EU to extra-EU routes is one of the principal concerns with the Fit for 55 policies, as it could lead to competitive distortions, as well as carbon leakage (as discussed below).

In addition to potential destination substitution by direct passengers, connecting passengers on a route between an EU and a non-EU destination may be more likely to switch their itinerary, as the airport at which their connection takes place has little effect on their overall journey.11 Fare increases on flights between two EU airports will be much greater than fare increases on flights between an EU airport and a non-EU airport. As such, the price of a connecting journey with a stop at an EU airport will be higher than one with a stop at a non-EU airport.

We find that the fares for connecting flights with a stop in the EU will increase by 2% in 2030, compared with just 0.2% for flights connecting through a non-EU airport. We estimate that these fare changes will lead to a fall in demand of 4% for connecting flights stopping at an EU airport, but an increase in demand of 3% for connecting flights stopping at a non-EU airport, due to passengers switching their itineraries.

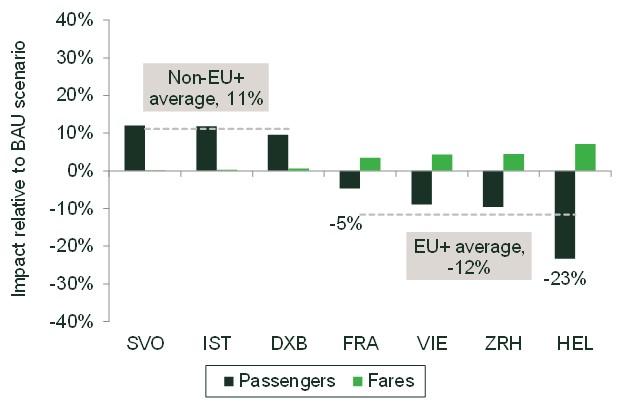

The impact on connecting passengers’ journey choices is more notable when looking at the different hub airports that can be used on a given route. For example, on the route between Hamburg and Bangkok in 2030, passenger numbers at non-EU hubs increase by 11%, while passenger numbers at EU hubs fall by 12%, as demonstrated in the figure below.

Figure 2 Changes to passenger numbers and fares for routes via largest hubs between Hamburg and Bangkok in 2030

Source: Oxera analysis.

Do the policies reduce emissions?

These results indicate that there will be reductions in demand on routes across Europe, which will in turn reduce emissions. However, there will also be some diversion of passengers to other routes, which will lead to increases in emissions.

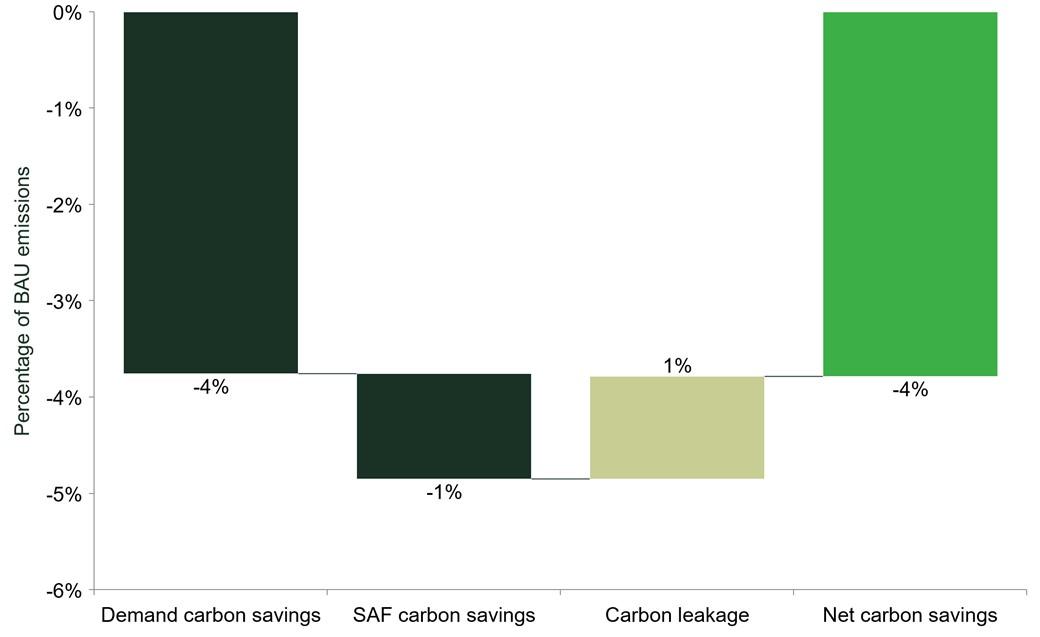

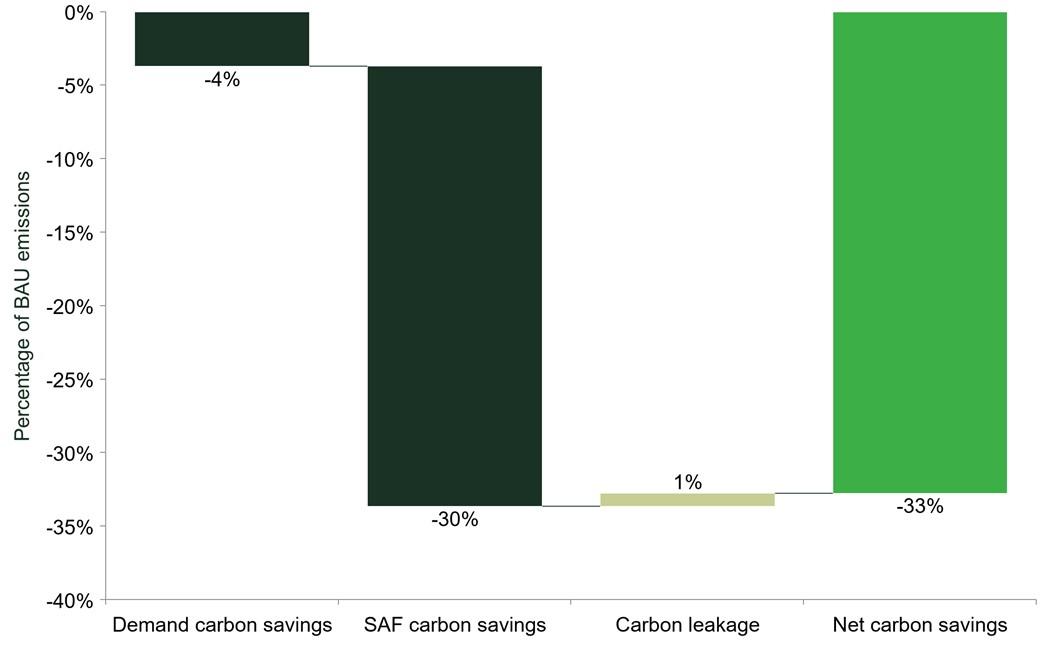

Overall, we find that the Fit for 55 policies will reduce emissions on direct flights by 4% relative to a scenario without such policies in 2030, and by 33% in 2050. Conversely, connecting routes will see emissions fall by only 2% in 2030 and 27% in 2050. The sources of the reductions are displayed below.

Figure 3 Effect of Fit for 55 proposals on carbon emissions on direct flights, 2030

Source: Oxera analysis.

Figure 4 Effect of Fit for 55 proposals on carbon emissions on direct flights, 2050

Source: Oxera analysis.

In 2030, the source of nearly all emissions reductions is from a decline in passenger demand, which is in contrast to much larger carbon savings from SAF in 2050. This is due to the roll-out of the ReFuelEU initiative, as only a small amount of SAF is mandated in 2030 (around 5%) compared with 2050 (63%), as the production and availability of SAF improves.

The results also indicate that there is an increase in emissions associated with passengers diverting to other destinations, which offsets the original savings—known as carbon leakage. We estimate that one-fifth of the emissions savings will be counteracted by the diversion of passengers to non-EU destinations in 2030.

What do these results mean for policymakers, the aviation sector and the climate?

The Fit for 55 policies will have a significant impact on the European aviation sector, affecting airlines’ networks, the services offered by airports, the fuels provided by suppliers, and the travel choices of consumers. However, our results indicate that a number of implications of these policies need to be considered in more detail.

Technology remains the critical unknown

Our findings indicate that the current design of the Fit for 55 policies does not reduce emissions to net zero by 2050 in the aviation sector, and that it achieves emissions reductions of only 4% in 2030 (against a target of 55%) and 33% in 2050 (against an effective target of 100%). While these targets include some offsetting to allow for residual emissions from aviation in 2050, if all else remains the same, the policies alone are unlikely to be sufficient to ensure that the sector achieves its targets.

These findings, however, are sensitive to assumptions around the development and roll-out of new fuels and technology. SAF take-up in the coming decades is still highly uncertain, with total emission savings dependant on the type of SAF used.12 Additionally, two potentially game-changing technologies in the aviation sector are electric and hydrogen-powered flights, when coupled with decarbonisation of the European energy grid. While most sources predict that these will not be viable until at least 2050, faster roll-out could lead to much greater emissions savings.

We have modelled different technological pathways to determine how a faster technological roll-out would affect overall emission reductions. We estimate that a faster roll-out of SAF, electric aircraft and hydrogen-powered flights will lead to greater savings than our baseline scenario (43% by 2050). However, subsidies may be needed to offset the high price currently faced by airlines purchasing SAF, and further research and investment in new technologies will be key to transforming European aviation and helping the sector’s transition to net zero.

Dealing with diversion

Another potential issue with the current design of the policies is carbon leakage, as some of the emissions that are saved as a result of the policies might be leaked as airlines use hubs outside the EU, or consumers change their destinations to airports outside the EU. We estimate that carbon leakage as a proportion of total emissions will be around 1% in both 2030 and 2050, but this makes up 22% of total emissions savings from the policies, and thus has the potential to undermine their efficacy.

In order for the sector to reach its emissions targets, more will need to be done to mitigate the risk of carbon leakage. One option is for the ETS to revert to its original scope, which would cover all flights originating or terminating in the EU. This would remove the incentive for flights originating or terminating in the EU to divert to non-EU destinations. As noted above, the Commission will revisit these policies in future, and the reversion of the ETS to its original scope has already been tabled as a possible change.

Interaction with other policies

The Fit for 55 policies sit alongside efforts by many countries to curb their emissions, particularly within the aviation sector. For example, in 2021 countries including Belgium, the Netherlands and Hungary introduced air passenger taxes on short-haul journeys, joining half a dozen countries that already applied aviation-specific taxes.

However, the major global initiative aimed at reducing emissions is ICAO’s CORSIA. The long-term scope of the ETS is dependent on the choices that ICAO makes over the baseline year for CORSIA and the robustness of its assessments of offsets. Additionally, there are questions around whether emissions that are offset, such as those covered under CORSIA, should be subject to policies such as the ETS and the ETD.

The non-CO2 impact of aviation on global warming

While the Commission has considered some non-CO2 impacts of the Fit for 55 policies (e.g. NOx and other gaseous emissions),13 not all environmental impacts from non-CO2 sources are taken into account.14 It is critical that there is a holistic assessment of all environmental impacts when determining the best way to decarbonise the aviation sector.

Is Fit for 55 enough?

The Fit for 55 policies are ambitious in their scope and represent a step change on previous climate policies outlined by the Commission. However, our analysis indicates that more may need to be done to limit passenger diversion, encourage SAF uptake, and stimulate technological developments in order to reach net zero by 2050. A supportive policy space and sufficient incentives should help to ensure that these ambitious and necessary targets can be reached.

1 We consider that the policy area (those jurisdictions where the Fit for 55 policies would be enacted) includes all EU27 member states, all members of the EEA and EFTA, and the UK, due to the similarity of policies in these areas. This is referred to as the EU+. European Commission (2021), ‘European Green Deal: Commission proposes transformation of EU economy and society to meet climate ambitions’, 14 July.

2 European Commission (2021), ‘Commission Staff Working Document Impact Assessment Report: Accompanying the document Proposal for a Directive of the European Parliament and of the Council amending Directive 2003/87/EC as regards aviation’s contribution to the Union’s economy-wide emission reduction target and appropriately implementing a global market-based measure’, 14 June, pp. 4–5.

3 The final legislation that enters into force is unlikely to be identical to the proposal.

4 See Oxera (2013), ‘The EU Emissions Trading Scheme: what are the options for reform?’, Agenda, 18 December (last accessed 24 August 2022); Oxera (2006), ‘European emissions trading: is it working?’, Agenda, 18 December (last accessed 24 August 2022); Oxera (2022), ‘Bidding for a more sustainable future: carbon trading in the EU’, Agenda, 30 March (last accessed 24 August 2022).

5 European Commission (2021), ‘Proposal for a Council Directive restructuring the Union framework for the taxation of energy products and electricity (recast)’, 14 July, p. 36.

6 To avoid tankering, airlines must ensure that the yearly quantity of aviation fuel uplifted at an EU airport is at least 90% of the yearly aviation fuel required. Additionally, there is a requirement that these quantities of SAF must be made available at all airports with more than 1m passengers annually. European Commission (2021), ‘Proposal for a regulation of the European Parliament and of the Council on ensuring a level playing field for sustainable air transport’, 2021/0205 (COD), 14 July, para. 22.

7 European Commission (2021), ‘Proposal for a regulation of the European Parliament and of the Council on the deployment of alternative fuels infrastructure, and repealing Directive 2014/94/EU of the European Parliament and of the Council’, 2021/0223 (COD), 14 July (last accessed 24 August 2022), p. 38.

8 CORSIA stands for Carbon Offsetting and Reduction Scheme for International Aviation. It has been developed by member states of the International Civil Aviation Organization (ICAO), an agency of the United Nations. For more information, see ICAO ENVIRONMENT, ‘Carbon Offsetting and Reduction Scheme for International Aviation’ (last accessed 24 August 2022).

9 European Commission (2021), ‘Proposal for a Directive of the European Parliament and of the Council amending Directive 2003/87/EC as regards aviation’s contribution to the Union’s economy-wide emission reduction target and appropriately implementing a global market-based measure’, 2021/0207 (COD), 14 July, (last accessed 24 August 2022), p. 13.

10 An intra-EU+ flight refers to a flight between two airports within our relevant policy area, as outlined above.

11 ‘Itinerary’ here refers to the choice of airports throughout their journey, including origin, connection and destination airports.

12 Fuels produced via the power-to-liquids (PtL) Fischer–Tropsch process, while possibly the cleanest available, are projected to make up only a very small proportion of fuel use in 2030. This further scaling to 2050 is crucial to cutting emissions, but remains highly uncertain.

13 European Commission (2021), ‘Commission Staff Working Document: Impact Assessment Accompanying the Proposal for a Regulation of the European Parliament and of the Council on ensuring a level playing field for sustainable air transport’, SWD/2021/633 final, 14 July (last accessed 13 June 2022), pp. 42–43.

14 These are largely made-up of contrails, which are the clouds of ice crystals that sometimes form in the wake of an aircraft flight at high altitude. Timmins, B. (2021), ‘Contrails: How tweaking flight plans can help the climate’, BBC News, 22 October (last accessed 16 June 2022). Please could you change that?

Related

Modernising EU competition policy: from guidelines to outcomes

This special edition of Top of the Agenda was recorded at our 2026 Brussels conference, which hosted senior figures from the European Commission, national competition authorities, academics and the legal community to discuss one of the most significant developments in EU competition policy in two decades: the revision of… Read More

When does a discount become deceptive? An economic framework for the regulation of reference pricing

The use of ‘reference’ pricing—where a previous (or future) ‘was’ price is displayed alongside the current ‘now’ price to indicate a discount for customers—is a common feature across digital and physical markets. In supermarkets, retailers commonly advertise a headline Recommended Retail Price (RRP), or ‘was’ price, alongside the current… Read More